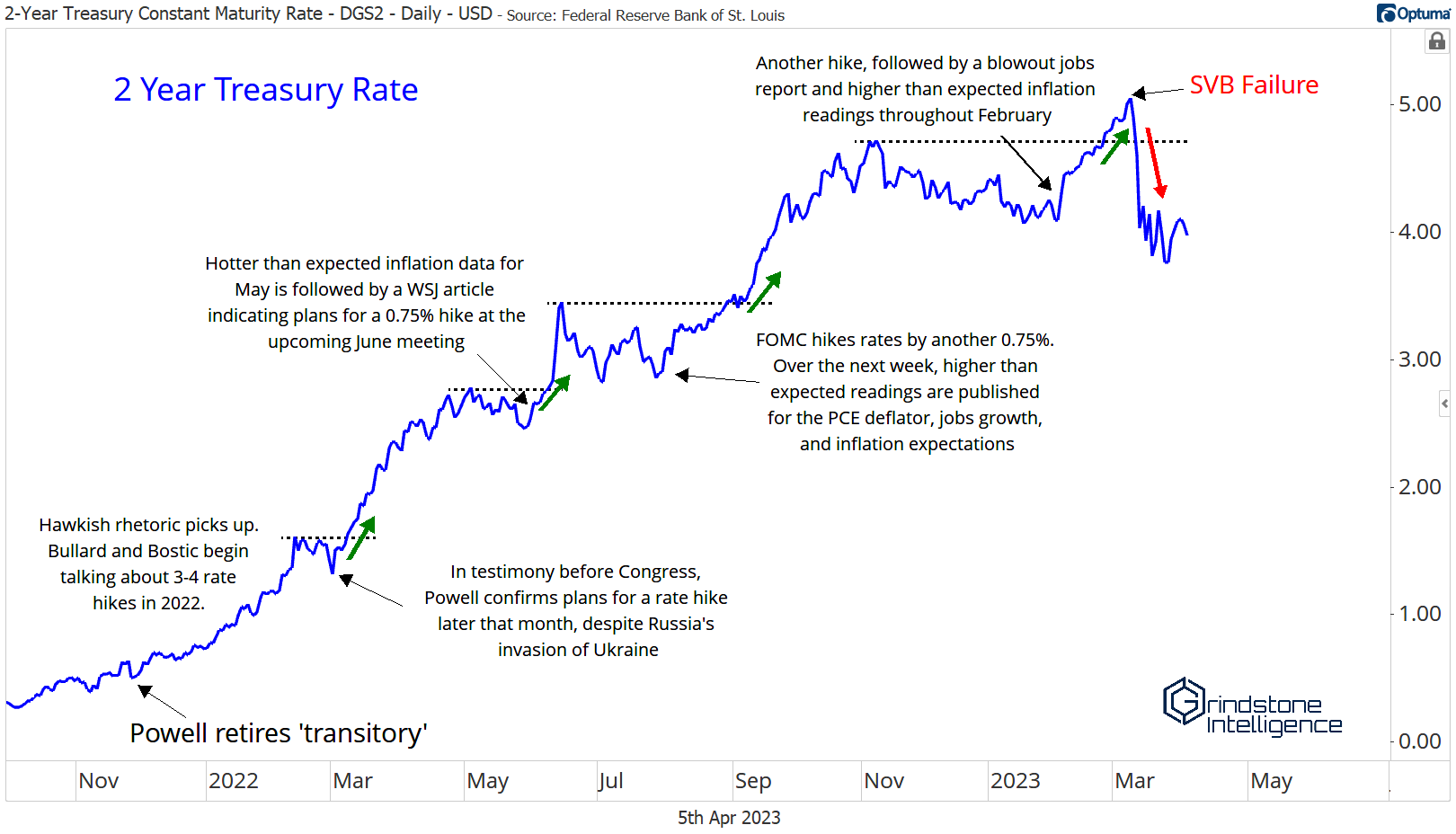

It’s starting to look as though interest rates have peaked, thanks in large part to the failure of Silicon Valley Bank.

In the weeks prior the banking crisis, every piece of economic data pointed to stubbornly high inflation and a tight labor market. That was the story driving Treasury yields higher all throughout 2022, and the latest batch of data pushed 2 year Treasury yields to the highest level since 2007.

In the weeks after the failure, though, 2 year rates have given back those gains and more.

Yields have fallen across the curve. Ten year Treasurys are breaking down to their lowest levels since last September.

Based solely on what we’ve witnessed over the last year, that would be a bad thing for the Dollar and a good thing for stocks. All throughout 2022 and into this new year, we watched as higher rates and a stronger Dollar pushed equities lower (and vice versa). Look at how closely the three moved together.

Will those relationship hold forever, though? Of course not. In fact, they’ve already begun to weaken.

The correlations between equity prices, rates, and currencies have rebounded from multi-decade extremes to something that more closely resembles an average.

Why might that be? Blame bank failures again.

Throughout 2022, lower rates reflected softening price pressures and bolstered hopes that the Fed could softly land a hot economy. Fears of a deep recession are the focus today. Deposits are flowing out of banks across the country and into money-market funds, and that disintermediation will force banks to pull back on credit issuance. Credit crunches often lead to deep recessions – a scenario which could force the Fed to lower rates.

But recessions just aren’t great news for stock prices, whether rates are coming down or not.