Do you remember when big tech was the ONLY place to invest?

Let’s rewind to the days before half the world closed its doors. From the end of 2018 to the pre-pandemic peak, the S&P 500 Information Technology Sector rose 65%. The Communication Services Sector, which sported 20% weights to both Alphabet and Facebook, jumped 40%. The S&P 500 itself climbed 35%. Not a bad year for investors, right? So long as they had their money in the right place, that is.

Over that 13 month period, every other sector underperformed the index.

Every market historian knows that the bulk of historical index returns are generated by a handful of names (that’s why we focus so much on identifying relative strength). Rarely, though, has that phenomenon been so readily apparent as it was that year, when more than 80% of sectors lagged the index.

COVID wasn’t the end of that story. In fact, forcing millions of people and their employers to embrace a digital transition was just gasoline on the fire. In the first 8 months of 2020, the Russell 1000 Growth index surged 45% relative to its Value counterpart.

Then came September 2020.

In just 3 days at the start of the month, growth stocks dropped 10%. Value fell only 4%. We couldn’t have known it at the time, but that day would mark the end of growth’s dominance. Value oriented stocks – especially in the Energy and Industrials sectors – have been in the driver’s seat ever since.

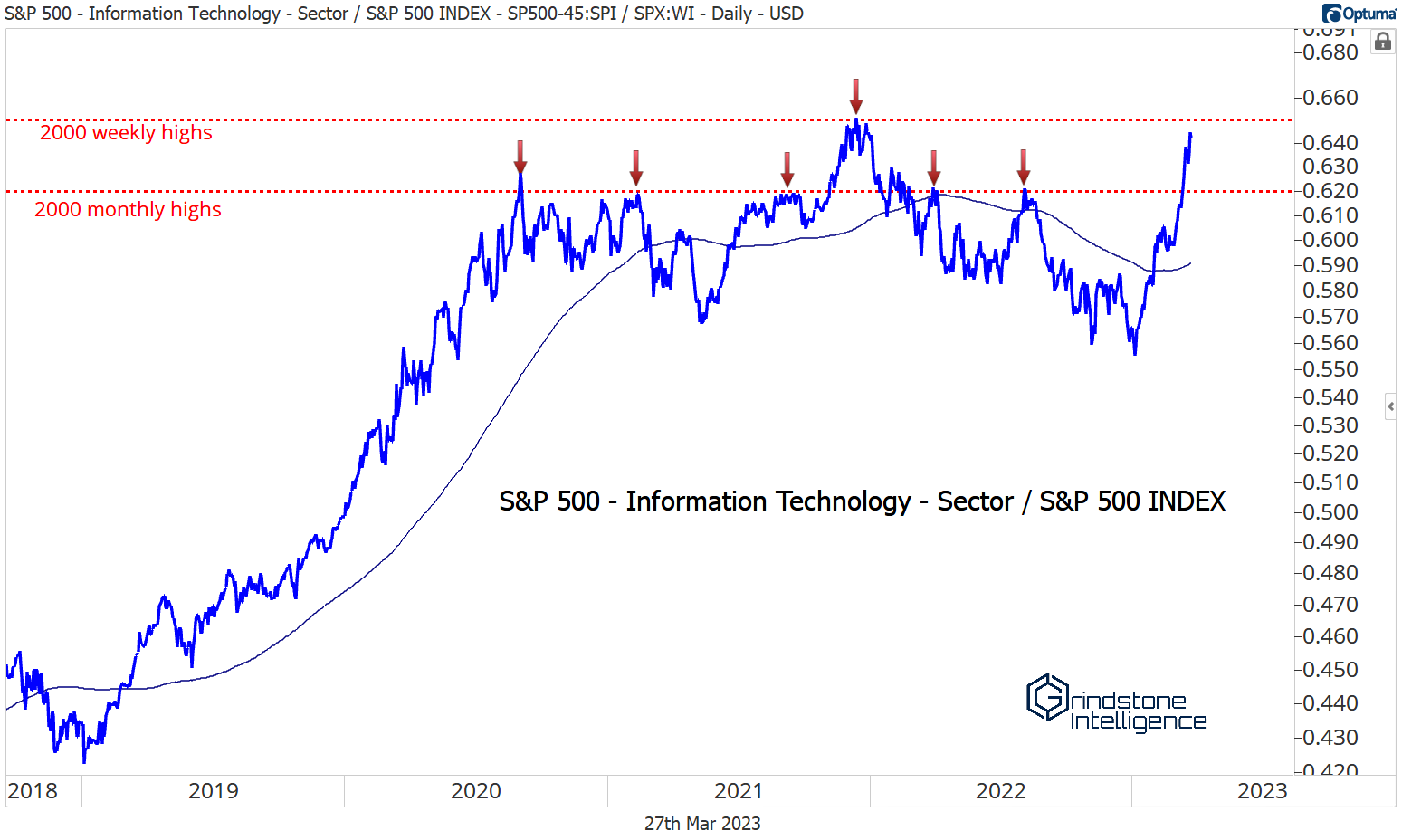

Big tech’s trouble couldn’t have started at a more logical place – the same place trouble began more than 20 years ago. Tech’s relative strength peaked exactly at the monthly highs from the internet bubble. Last time, it resulted in an 80% collapse for the sector, and a run of lackluster performance that didn’t reverse until the financial crisis. The question is, will history repeat itself?

The answer may rest on the path of interest rates. Financial assets have benefited from 40 years of falling interest rates since the early 1980s. Not only have lower rates reduced borrowing costs and helped drive economic expansion, they’ve also forced investors out the risk spectrum. An investor that once was happy with a risk-free Treasury yielding 6% hasn’t had that option since the turn of the century. Instead, they’ve had to allocate funds towards riskier asset classes – high yield bonds, real estate, stocks, etc. And because interest rates are a primary component of the discount rate used to estimate the value of most assets, stocks with higher long-term growth expectations have disproportionately benefited.

That 40-year run for rates may be at an end, though. With inflation far above the Federal Reserve’s 2% target, they’ve raised short-term borrowing costs at 9 consecutive meetings since last March. Interest rates across the curve have risen to levels not seen since the Financial Crisis.

Growth stocks felt the consequences in 2022. Information Technology, Communication Services, and Consumer Discretionary (dominated by Amazon and Tesla) were all leaders on the downside. Value and risk-off sectors, meanwhile, held up significantly better.

In 2023, though, the narrative has reversed. Tech, Communications, and Discretionary are each up double digits, while everyone else is in the red.

Interest rates again are largely to blame. The 10-Year Treasury yield has retreated from last year’s highs and is threatening to fall below support. If it does, big tech is set to remain in the driver’s seat.

Besides a resurgence in yields, what’s the biggest risk to this narrative? The ‘why’ of interest rates breaking down.

In the first few months of the year, economists and investors began to believe the Federal Reserve was close to achieving a so-called ‘soft landing’, i.e. controlling inflation without causing a recession. If so, rate hikes would soon be at an end, and investors could be more confident in valuing a growing company’s prospects.

With the failure of Silicon Valley and Signature Bank, though, that soft landing scenario seems unlikely. Deposits are flowing out of banks across the country and into money-market funds, and banks will almost certainly respond by pulling back on credit issuance. Those types of credit crunches often lead to recession.

Markets have responded by pricing in a series of rate cuts by the Fed in the back half of this year, and the prospect of lower rates brings with it all those growth stock tailwinds of the 2010s. While Financials, Industrials, Energy, and Materials sectors have all dropped since SVB’s collapse, Tech, Communications, and Discretionary are doing just fine.

The question is, will Powell & Co. play along? Powell isn’t forecasting cuts this year, and neither are his colleagues. But they don’t sound too confident in a soft landing either. Instead, they continue to point towards the risks of removing restrictive policy too early, lest they repeat the mistakes of the 1970s. Their mandate is to maintain price stability and full employment, and they can’t achieve the latter without first ensuring the former. In other words, Powell’s Fed may not offer the same monetary support that we’ve grown accustomed to during recent recessions.

If that’s the case, it may not matter which sectors are showing relative strength – they’ll all be facing some serious pressure. Bear markets that coincide with recessions often take years to find a bottom. And you’d be hard-pressed to find one that’s bottomed before the recession even began. That’s the crux of the bear case for stocks.

Here’s one final chart to chew on: Tech is back above those monthly, internet bubble highs, and it’s set to challenge the weekly level.

If Information Technology, the biggest sector in the index, is setting new all-time relative highs… well, good luck defending that bear case.